Risk of Home Builder Credit Defaults

{kind=link}

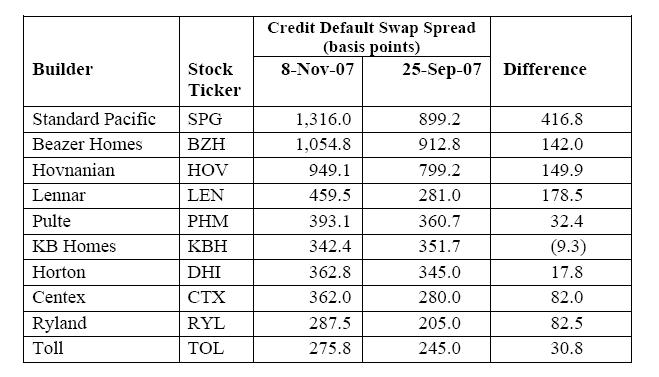

Based on pricing for credit default swaps, the market now perceives an increasing potential for defaults on bonds issued by three major public homebuilders: Standard Pacific, Beazer and Hovnanian.[1] There are also smaller but significant recent increases in default risk across the entire housing sector.

According to Michael Shedlock (see his blog at globaleconomicanalysis.blogspot.com), the market perception was much more positive at the end of the first quarter of 2007. All of these builders then had credit default swap spreads in the neighborhood of 200 basis points.

The chart below shows how the market perceived default risk of selected publicly traded homebuilders on November 8, 2007 as compared to September 25, 2007 as reflected in the difference between the credit default swap spread on those two dates.[2]

[1] For 2006, Builder Magazine ranked Standard Pacific as # 11, Beazer as #7 and Hovnanian as #6, based on unit closings.

[2] A company’s credit default swap spread is the annual cost of protection against a default by the company. The information reflected in the chart is taken from Michael “Mish” Shedlock’s blog at: http://globaleconomicanalysis.blogspot.com/2007/11/homebuilder-credit-default-swaps.html